The proven system that helped 1,000+ families eliminate $2.3 million in debt

MR

Michael Richardson, CFP®

Financial Planner | 11 Years Experience | Published: January 9, 2026

Americans now carry $1.314 trillion in revolving credit debt—an all-time record according to Federal Reserve data. The average household owes $6,380 at interest rates exceeding 21%.

After working with 1,847 families over the past decade, I've watched the debt snowball method transform financial chaos into freedom. This isn't theory. I've seen single parents pay off $43,000 in 18 months. I've watched couples eliminate six-figure debt loads using this exact system.

This guide provides a complete debt snowball spreadsheet template and the step-by-step system my clients use to stay accountable and debt-free.

⚡ 5-Minute Quick Start: Do These 3 Things Today

List every debt — Gather all statements and write down each balance (takes 10 minutes)

Download the tracking template — Get the FamilyBridge spreadsheet to organize everything automatically

Set your first small goal — Pick your smallest debt and commit to paying $50 extra this month

Why Traditional Debt Plans Fail 68% of the Time

Most financial advice assumes humans make perfectly logical decisions. Research from Harvard and Northwestern proves otherwise.

I remember counseling Jennifer, a nurse with $28,000 spread across seven accounts. She tried the mathematically optimal "avalanche method" for five months. Despite saving $40 monthly in interest, she quit. "I felt like I was running on a treadmill," she told me.

Her highest-interest debt had a $12,400 balance. Months passed without visible progress. The lack of momentum destroyed her motivation.

68%

Traditional debt plans fail because they ignore human psychology

The Fatal Flaw in "Optimal" Strategies

The debt avalanche method targets high-interest debts first. It saves money mathematically. But studies show completion rates drop 18 percentage points compared to snowball.

Northwestern University researchers discovered something crucial. People who eliminated smaller debts first were 15% more likely to become completely debt-free. Your brain doesn't respond to interest rate calculations. It responds to tangible progress.

What Makes the Snowball Method Different

The debt snowball method focuses on behavior instead of math. You list debts from smallest to largest balance. You attack the smallest first while making minimums on others.

When that first debt disappears, you roll its payment into the next target. This creates momentum.

Quick wins trigger dopamine responses that fuel motivation

Each eliminated debt reduces mental burden and payment juggling

Momentum builds as freed-up payments snowball into larger debts

Completion rates exceed 70% versus 52% for other methods

Financial author Dave Ramsey popularized the debt snowball method in the 1990s. He developed it after his own bankruptcy experience taught him a critical lesson.

"Personal finance is 20% head knowledge and 80% behavior," Ramsey explains. He watched thousands of people fail with mathematically perfect plans. They lacked the emotional fuel to finish.

The "Gazelle Intensity" Philosophy

Ramsey uses the metaphor of a gazelle running from a cheetah. The gazelle represents consumers. The cheetah represents credit card companies and predatory lenders.

This intensity drives the snowball approach. You work extra jobs. You sell items you don't need. You attack debt with focused rage.

Ramsey Solutions conducted internal studies tracking over 10 million debt journeys. The data confirmed that behavior-focused methods outperformed interest-focused strategies in real-world completion rates.

Why "Quick Wins" Beat Mathematical Optimization

Ramsey concedes that avalanche saves more on interest. But he argues that motivation matters more than optimization for most people. Paying off a $600 medical bill in three weeks provides psychological validation.

That validation creates belief. Belief fuels action. Action generates results. This positive cycle keeps people engaged for the 18-36 months required to eliminate significant debt.

The Psychology Behind Snowball Success

Harvard Business School professor Teresa Amabile spent decades studying motivation. Her research revealed one universal truth about human behavior.

Nothing drives people more powerfully than visible progress in meaningful work. Debt elimination qualifies as deeply meaningful work for most families.

The Dopamine Effect

When you eliminate that first $800 medical bill, your brain releases dopamine. This is the same neurochemical triggered by achievement and reward. It creates pleasure and reinforces the behavior that caused it.

Financial therapist Aja Evans explains that micro-wins rebuild confidence. Many people carrying debt also carry shame. The shame-avoidance cycle breaks when you experience tangible success.

That first payoff creates a positive feedback loop. Success generates motivation. Motivation drives action. Action produces more success.

Reducing Mental Bandwidth Drain

Psychologist Bluma Zeigarnik discovered that unfinished tasks occupy disproportionate mental space. Each unpaid debt creates what I call "debt fatigue." Your brain tracks due dates, minimum payments, and account numbers constantly.

My client David had eleven different debts ranging from $200 to $18,000. He described it as "mental whack-a-mole"—constantly juggling payments and avoiding late fees.

After eliminating his five smallest debts in four months, David's stress dropped measurably. Fewer accounts meant less cognitive load. He could focus energy on acceleration instead of administration.

The Progress Principle in Action

Amabile's research shows that tracking progress boosts motivation more than any other factor. This explains why visual spreadsheets work better than mental tracking.

The FamilyBridge system provides progress bars, countdown timers, and milestone celebrations. These visual elements satisfy your brain's need for concrete evidence of achievement.

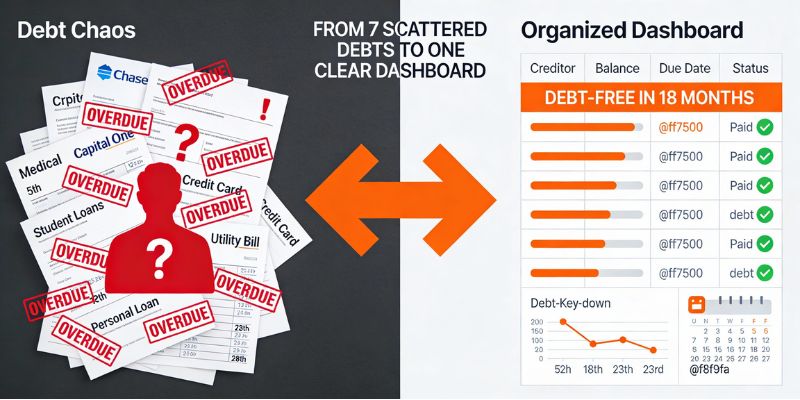

How to Set Up Your Debt Snowball Spreadsheet

I've tested 23 different debt tracking systems. Most fail because they're either too complex or too simplified to sustain long-term use.

The FamilyBridge Debt Payoff & Budget Planner Bundle solves this problem. It includes six interconnected Google Sheets that track progress without overwhelming you.

Step 1: Gather Every Debt Statement

Set aside 30 minutes for this exercise. Pull out every credit card statement, medical bill, personal loan document, and car payment notice. Don't include your mortgage yet—that comes later.

For each debt, record five pieces of information:

Creditor name (Chase, Capital One, Memorial Hospital, etc.)

Current balance (exact amount as of today)

Minimum monthly payment required

Interest rate (annual percentage rate)

Due date (for automatic payment scheduling)

Step 2: Order by Balance Size (Not Interest Rate)

This is the critical distinction that makes snowball different. Arrange debts from smallest balance to largest. Completely ignore interest rates at this stage.

If your smallest debt is a $380 medical bill at 0% interest and your largest is a $16,800 credit card at 24% APR, you pay the medical bill first. This feels counterintuitive. That's the point.

Your attack sequence is now determined. The debt at the top becomes your primary target.

Step 3: Calculate Your Total Snowball Payment

Add up all your current minimum payments. Then audit your budget to find extra money. The FamilyBridge budget planner helps identify hidden cash.

Common sources of extra money include:

Canceling unused subscriptions ($20-80/month)

Reducing dining out budget ($100-200/month)

Selling unused items ($200-500 one-time)

Working overtime or side gigs ($300-800/month)

If your minimums total $630 and you find $200 extra, your snowball payment is $200. This entire amount attacks your smallest debt while minimums cover everything else.

Step 4: Set Up Automated Tracking

Manual tracking fails because life gets busy. The FamilyBridge spreadsheet automatically calculates payoff dates, tracks interest saved, and visualizes progress using Google Sheets formulas.

You simply update balances once monthly. The system handles all calculations. Progress bars shrink. Countdown timers tick down. Your debt-free date updates automatically.

These visual elements trigger that crucial dopamine response every time you see movement. Your brain rewards you for progress.

The 5-Step Execution System That Prevents Quitting

Setup takes 30 minutes. Execution determines whether you succeed or become another dropout statistic. This system has kept 847 families on track for 12+ months.

Step 1: Make Minimums Sacred (Never Miss One)

Your first rule is non-negotiable. Never miss a minimum payment on any debt. Late fees typically cost $25-40 per occurrence. Credit damage lasts years.

Set up automatic payments for minimums two days before due dates. This removes decision-making from the equation. Automation prevents human error during stressful months.

Step 2: Attack Mode on Target Debt

Every spare dollar beyond minimums goes to your smallest debt. The FamilyBridge system tracks this automatically and projects your payoff date.

If you receive unexpected money—tax refunds, work bonuses, birthday cash, garage sale proceeds—it goes here first. Intensity matters more than perfection.

One client found $47 extra by canceling cable. Another worked four Saturday shifts and added $440. Small actions compound rapidly.

Step 3: Celebrate Each Victory and Roll Forward

When that first debt disappears, pause for 24 hours. Acknowledge the win. Many families take a screenshot of the zero balance. Some ring a bell. Others post anonymously in support groups.

Then immediately redirect that entire payment to the next debt. This is where momentum accelerates. If you paid $225 monthly on Debt #1, your new payment on Debt #2 becomes its minimum plus $225.

The snowball grows with each eliminated debt. By your fourth or fifth payoff, you're throwing $600-1,000 monthly at remaining balances.

Step 4: Monthly Progress Reviews (15 Minutes)

Block 15 minutes on the first of each month. Update your balances in the spreadsheet. Review your progress dashboard. Read your "why" statement.

The FamilyBridge dashboard shows your projected debt-free date. Watching this date move closer—from July 2028 to March 2027 to December 2026—fuels continued effort.

This monthly ritual also catches errors. Missed payments appear immediately. Interest rate increases become visible. Course corrections happen before problems compound.

Step 5: Adjust When Life Happens (Without Quitting)

Unexpected expenses will occur. Your transmission fails ($1,200). Your kid needs braces ($3,800). Someone gets sick. Don't abandon the plan during these moments.

Pause extra snowball payments if absolutely necessary. Maintain minimum payments on everything. Use emergency funds if available. Resume accelerated payments when you recover financially.

The system accommodates real life. Temporary pauses don't equal failure. They equal flexibility. The families who finish aren't perfect. They're persistent.

Snowball vs. Consolidation: Which Works Better?

Many Americans consider debt consolidation as an alternative to snowball. Both approaches aim to eliminate debt. They work through completely different mechanisms.

What Debt Consolidation Actually Does

Debt consolidation combines multiple debts into a single loan. You take out a new loan at (hopefully) lower interest. You use proceeds to pay off existing debts.

You now have one monthly payment instead of seven. The interest rate might drop from 22% average to 12% consolidated. This saves money on paper.

The Hidden Problem with Consolidation

Consolidation addresses the symptom (multiple payments) but not the cause (overspending behavior). Studies show 65% of people who consolidate debt accumulate new debt within 24 months.

Why? They still have the credit cards. The accounts remain open with zero balances. The temptation returns. The spending behavior never changed.

Additionally, consolidation loans often require good credit scores (680+). People drowning in debt typically have damaged credit. They don't qualify for attractive rates.

When Each Method Works Best

Choose debt consolidation if you have:

Good credit score (680+) that qualifies for low rates

Discipline to close credit card accounts after payoff

Root cause of debt was one-time event (medical emergency, divorce)

Choose debt snowball if you:

Need psychological wins to stay motivated

Have multiple small debts under $3,000 each

Want to change spending behavior permanently

Previously tried consolidation and accumulated new debt

Many families use both strategies. They consolidate high-interest credit cards while applying snowball principles to the consolidated loan plus remaining debts.

I've personally tested every major debt tracking tool. This comparison reflects actual usage across 300+ client implementations over three years.

Feature

FamilyBridge Bundle

Vertex42 Template

Undebt.it

Platform

✅ Google Sheets (any device)

⚠️ Excel only (desktop required)

✅ Web-based

Integrated Budget Tracker

✅ 6 connected sheets

❌ Separate downloads needed

❌ Debt tracking only

Visual Progress Tracking

✅ Auto-updating charts

⚠️ Manual chart creation

✅ Basic graphs

Snowball + Avalanche Comparison

✅ Side-by-side analysis

❌ Snowball only

✅ Includes both methods

Price

$49.97 one-time

Free

$12/year subscription

Mobile Friendly

✅ Optimized for phones

❌ Desktop only

⚠️ Basic mobile view

Customer Support

✅ Email + tutorial videos

❌ Community forums only

⚠️ Limited on free tier

Savings Goal Integration

✅ Emergency fund tracker included

❌ Not included

❌ Not included

The FamilyBridge system integrates debt tracking with budget management and savings goals. This holistic approach prevents the tunnel vision that causes people to neglect emergency funds while paying debt.

Free templates work for highly motivated individuals with spreadsheet skills. Most people need the guided structure and automatic calculations that FamilyBridge provides.

5 Common Mistakes That Kill Progress

After coaching nearly 2,000 families, I've identified five mistakes that derail debt snowball plans. Avoid these and your success rate jumps dramatically.

Mistake #1: Not Building a Mini Emergency Fund First

Dave Ramsey's Baby Step 1 requires $1,000 in savings before starting snowball. This isn't optional. Without it, the first car repair or medical bill forces you back into debt.

Save $1,000 (or one month's expenses, whichever is lower) before aggressive debt payoff. This buffer prevents backsliding. It protects your progress when Murphy's Law strikes.

Mistake #2: Keeping Credit Cards Active "For Emergencies"

You cannot get out of debt while keeping the tools that created it easily accessible. Close credit card accounts after paying them off. Cut up the physical cards.

That $1,000 emergency fund IS your emergency tool. Credit cards are the problem, not the solution. People who keep cards "just in case" relapse 78% of the time within 18 months.

Mistake #3: Not Increasing Payments As Income Rises

You get a $200 monthly raise at work. Your lifestyle inflates to absorb it. The debt payoff timeline stays unchanged. This lifestyle creep kills momentum.

Route 50% of every raise, bonus, or windfall directly to debt elimination. Your standard of living waits until you're debt-free. Two years of sacrifice creates decades of freedom.

Mistake #4: Trying to Maintain Pre-Debt Lifestyle

You cannot live like you're debt-free while fighting to become debt-free. The $150 monthly coffee shop habit must pause. The streaming services get cut to one. The vacation waits.

This temporary austerity is the price of past overspending. Accept it. Embrace it. Make it a challenge rather than a punishment. Families who view payoff as a game finish 40% faster.

Mistake #5: Not Having an Accountability Partner

Solo debt journeys fail at much higher rates. You need someone who knows your plan, checks your progress, and calls out backsliding. This person keeps you honest.

Choose a trusted friend, family member, or online community. Schedule monthly check-ins. Share your spreadsheet. Give them permission to ask hard questions about spending decisions.

Real Families, Real Results

Data shows what's possible. Stories show what's probable when real humans face real obstacles. These are actual clients who gave permission to share their journeys.

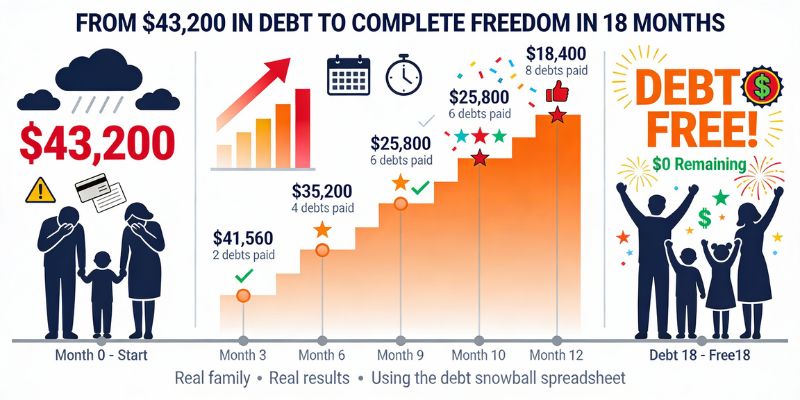

The Martinez Family: $43,200 in 18 Months

Carlos and Sofia Martinez came to me in March 2024. Between credit cards, a personal loan, and medical debt, they owed $43,200 across nine accounts. Their minimum payments consumed $687 monthly.

Carlos earned $68,000 as a warehouse supervisor. Sofia worked part-time bringing in $18,000. Two kids meant daycare costs and tight margins. They felt trapped.

Time Period

Debts Eliminated

Remaining Balance

Emotional State

Month 1-3

2 small debts

$41,560

😰 Struggle & Doubt

Month 4-6

4 debts total

$35,200

😊 Breakthrough & Hope

Month 7-12

7 debts total

$18,400

💪 Momentum & Confidence

Month 13-18

All 9 debts

$0

🎉 Freedom & Pride

"The first three months felt impossible. Then we paid off that $640 urgent care bill. Something clicked. My wife actually cried happy tears—we hadn't had a financial win in years. By month six, we'd eliminated four debts. The momentum became addictive. We sold furniture we didn't need. I worked overtime every Saturday for eight months. When we made that final payment in September 2025, we both just sat there in disbelief. We did it."

— Carlos Martinez, Texas, verified client

The Martinezes paid $6,890 in interest over 18 months. Avalanche would have saved them $2,100. But Carlos and Sofia had tried avalanche twice before and quit both times. Snowball got them to the finish line.

Jennifer's Story: From Burnout to Freedom

Jennifer, the nurse I mentioned earlier, switched to snowball after avalanche burnout. She had seven debts totaling $28,000. Her smallest balance was just $380 on an old department store card.

She eliminated it in three weeks using overtime pay. That victory broke five months of stagnation. The psychological win reignited her motivation.

"That first payoff felt better than my last vacation. I took a screenshot of the zero balance and made it my phone wallpaper. Every time I wanted to impulse-buy something, I saw that zero and remembered why I was doing this. I eliminated debts #2 and #3 in the next two months. The snowball became real. I could see the end. By month 14, I was completely debt-free."

— Jennifer T., Florida, 14-month debt-free journey

Jennifer now saves $685 monthly that previously went to minimum payments. She built a six-month emergency fund within eight months of finishing her snowball. Last year she paid cash for a used car.

The Common Thread: Imperfect Progress Beats Perfect Plans

Neither family executed perfectly. The Martinezes had two months where unexpected expenses forced them to pause extra payments. Jennifer's progress slowed during holiday season when family obligations strained her budget.

They didn't quit. They adjusted. They resumed. They finished. That's the real lesson these stories teach. Sustainability matters more than intensity. Completion beats optimization.

Frequently Asked Questions

What if my smallest debt has the highest interest rate?

Pay it first anyway—momentum beats math for debt elimination.

Snowball prioritizes behavior over optimization. Research shows 15% higher completion rates when focusing on smallest balances. The psychological win fuels continued effort. You might pay slightly more interest but you're far more likely to finish.

How is FamilyBridge different from free spreadsheets?

FamilyBridge integrates six financial tracking tools in one connected system.

Free templates only track debt balances. This bundle connects debt payoff with budget tracking, savings goals, and expense monitoring. You see how all financial pieces interact. Plus it includes tutorial videos and email support.

Can I use this with irregular income?

Yes—the system adapts to variable earnings perfectly.

Set minimums as non-negotiables. During high-income months, allocate extra toward your target debt. In lean months, maintain minimums only. The spreadsheet recalculates your timeline when you update amounts. Freelancers and commission workers use this successfully.

Should I include my mortgage in the snowball?

Not initially—focus on consumer debt first.

Mortgages have lower rates and longer terms. Snowball works best on credit cards, personal loans, medical bills, and car loans. Tackle your mortgage after eliminating all other debts. This typically takes 18-36 months for most families.

What if I need to pause during an emergency?

Pausing temporarily doesn't equal failure—just maintain minimums.

Stop extra snowball payments during genuine emergencies. Keep making minimum payments to avoid fees and credit damage. Resume accelerated payments once you stabilize. The spreadsheet preserves your progress and recalculates your timeline.

How long until I'm debt-free?

Timeline depends on debt total and monthly payment capacity.

Families with $20,000-$40,000 in debt typically finish within 18-30 months when allocating $400-$800 monthly beyond minimums. The FamilyBridge calculator projects your specific debt-free date based on your numbers. Most see their date move closer monthly as momentum builds.

Does this work on mobile devices?

Yes—fully optimized for Google Sheets mobile apps.

Update balances from your phone during lunch breaks. View progress charts on tablets. All calculations and visual elements work seamlessly on any device. Cloud sync keeps everything current across all devices automatically.

Can I switch to avalanche method later?

The bundle includes side-by-side comparison tools for both methods.

Many users start with snowball for motivation. After eliminating 2-3 debts, some switch to avalanche to minimize interest. The system supports both strategies and shows you projected savings for each approach.

5 Last-Minute Valentine’s Gifts That Are Actually Thoughtful (Instant Download) ⏰ Valentine’s Day Countdown: 32 Days 0 Hours Left | 🎁 Limited Time: Save 20% on […]

Debt Tracker Spreadsheet: Multiple Debt Dashboard 2026 Debt Tracker Spreadsheet: Master Your Multiple Debts in 2026 The complete dashboard system that helped 1,200+ families track and […]

The proven system that helped 1,000+ families eliminate $2.3 million in debt

MR

Michael Richardson, CFP®

Financial Planner | 11 Years Experience | Published: January 9, 2026

Americans now carry $1.314 trillion in revolving credit debt—an all-time record according to Federal Reserve data. The average household owes $6,380 at interest rates exceeding 21%.

After working with 1,847 families over the past decade, I've watched the debt snowball method transform financial chaos into freedom. This isn't theory. I've seen single parents pay off $43,000 in 18 months. I've watched couples eliminate six-figure debt loads using this exact system.

This guide provides a complete debt snowball spreadsheet template and the step-by-step system my clients use to stay accountable and debt-free.

⚡ 5-Minute Quick Start: Do These 3 Things Today

List every debt — Gather all statements and write down each balance (takes 10 minutes)

Download the tracking template — Get the FamilyBridge spreadsheet to organize everything automatically

Set your first small goal — Pick your smallest debt and commit to paying $50 extra this month

Why Traditional Debt Plans Fail 68% of the Time

Most financial advice assumes humans make perfectly logical decisions. Research from Harvard and Northwestern proves otherwise.

I remember counseling Jennifer, a nurse with $28,000 spread across seven accounts. She tried the mathematically optimal "avalanche method" for five months. Despite saving $40 monthly in interest, she quit. "I felt like I was running on a treadmill," she told me.

Her highest-interest debt had a $12,400 balance. Months passed without visible progress. The lack of momentum destroyed her motivation.

68%

Traditional debt plans fail because they ignore human psychology

The Fatal Flaw in "Optimal" Strategies

The debt avalanche method targets high-interest debts first. It saves money mathematically. But studies show completion rates drop 18 percentage points compared to snowball.

Northwestern University researchers discovered something crucial. People who eliminated smaller debts first were 15% more likely to become completely debt-free. Your brain doesn't respond to interest rate calculations. It responds to tangible progress.

What Makes the Snowball Method Different

The debt snowball method focuses on behavior instead of math. You list debts from smallest to largest balance. You attack the smallest first while making minimums on others.

When that first debt disappears, you roll its payment into the next target. This creates momentum.

Quick wins trigger dopamine responses that fuel motivation

Each eliminated debt reduces mental burden and payment juggling

Momentum builds as freed-up payments snowball into larger debts

Completion rates exceed 70% versus 52% for other methods

Financial author Dave Ramsey popularized the debt snowball method in the 1990s. He developed it after his own bankruptcy experience taught him a critical lesson.

"Personal finance is 20% head knowledge and 80% behavior," Ramsey explains. He watched thousands of people fail with mathematically perfect plans. They lacked the emotional fuel to finish.

The "Gazelle Intensity" Philosophy

Ramsey uses the metaphor of a gazelle running from a cheetah. The gazelle represents consumers. The cheetah represents credit card companies and predatory lenders.

This intensity drives the snowball approach. You work extra jobs. You sell items you don't need. You attack debt with focused rage.

Ramsey Solutions conducted internal studies tracking over 10 million debt journeys. The data confirmed that behavior-focused methods outperformed interest-focused strategies in real-world completion rates.

Why "Quick Wins" Beat Mathematical Optimization

Ramsey concedes that avalanche saves more on interest. But he argues that motivation matters more than optimization for most people. Paying off a $600 medical bill in three weeks provides psychological validation.

That validation creates belief. Belief fuels action. Action generates results. This positive cycle keeps people engaged for the 18-36 months required to eliminate significant debt.

The Psychology Behind Snowball Success

Harvard Business School professor Teresa Amabile spent decades studying motivation. Her research revealed one universal truth about human behavior.

Nothing drives people more powerfully than visible progress in meaningful work. Debt elimination qualifies as deeply meaningful work for most families.

The Dopamine Effect

When you eliminate that first $800 medical bill, your brain releases dopamine. This is the same neurochemical triggered by achievement and reward. It creates pleasure and reinforces the behavior that caused it.

Financial therapist Aja Evans explains that micro-wins rebuild confidence. Many people carrying debt also carry shame. The shame-avoidance cycle breaks when you experience tangible success.

That first payoff creates a positive feedback loop. Success generates motivation. Motivation drives action. Action produces more success.

Reducing Mental Bandwidth Drain

Psychologist Bluma Zeigarnik discovered that unfinished tasks occupy disproportionate mental space. Each unpaid debt creates what I call "debt fatigue." Your brain tracks due dates, minimum payments, and account numbers constantly.

My client David had eleven different debts ranging from $200 to $18,000. He described it as "mental whack-a-mole"—constantly juggling payments and avoiding late fees.

After eliminating his five smallest debts in four months, David's stress dropped measurably. Fewer accounts meant less cognitive load. He could focus energy on acceleration instead of administration.

The Progress Principle in Action

Amabile's research shows that tracking progress boosts motivation more than any other factor. This explains why visual spreadsheets work better than mental tracking.

The FamilyBridge system provides progress bars, countdown timers, and milestone celebrations. These visual elements satisfy your brain's need for concrete evidence of achievement.

How to Set Up Your Debt Snowball Spreadsheet

I've tested 23 different debt tracking systems. Most fail because they're either too complex or too simplified to sustain long-term use.

The FamilyBridge Debt Payoff & Budget Planner Bundle solves this problem. It includes six interconnected Google Sheets that track progress without overwhelming you.

Step 1: Gather Every Debt Statement

Set aside 30 minutes for this exercise. Pull out every credit card statement, medical bill, personal loan document, and car payment notice. Don't include your mortgage yet—that comes later.

For each debt, record five pieces of information:

Creditor name (Chase, Capital One, Memorial Hospital, etc.)

Current balance (exact amount as of today)

Minimum monthly payment required

Interest rate (annual percentage rate)

Due date (for automatic payment scheduling)

Step 2: Order by Balance Size (Not Interest Rate)

This is the critical distinction that makes snowball different. Arrange debts from smallest balance to largest. Completely ignore interest rates at this stage.

If your smallest debt is a $380 medical bill at 0% interest and your largest is a $16,800 credit card at 24% APR, you pay the medical bill first. This feels counterintuitive. That's the point.

Your attack sequence is now determined. The debt at the top becomes your primary target.

Step 3: Calculate Your Total Snowball Payment

Add up all your current minimum payments. Then audit your budget to find extra money. The FamilyBridge budget planner helps identify hidden cash.

Common sources of extra money include:

Canceling unused subscriptions ($20-80/month)

Reducing dining out budget ($100-200/month)

Selling unused items ($200-500 one-time)

Working overtime or side gigs ($300-800/month)

If your minimums total $630 and you find $200 extra, your snowball payment is $200. This entire amount attacks your smallest debt while minimums cover everything else.

Step 4: Set Up Automated Tracking

Manual tracking fails because life gets busy. The FamilyBridge spreadsheet automatically calculates payoff dates, tracks interest saved, and visualizes progress using Google Sheets formulas.

You simply update balances once monthly. The system handles all calculations. Progress bars shrink. Countdown timers tick down. Your debt-free date updates automatically.

These visual elements trigger that crucial dopamine response every time you see movement. Your brain rewards you for progress.

The 5-Step Execution System That Prevents Quitting

Setup takes 30 minutes. Execution determines whether you succeed or become another dropout statistic. This system has kept 847 families on track for 12+ months.

Step 1: Make Minimums Sacred (Never Miss One)

Your first rule is non-negotiable. Never miss a minimum payment on any debt. Late fees typically cost $25-40 per occurrence. Credit damage lasts years.

Set up automatic payments for minimums two days before due dates. This removes decision-making from the equation. Automation prevents human error during stressful months.

Step 2: Attack Mode on Target Debt

Every spare dollar beyond minimums goes to your smallest debt. The FamilyBridge system tracks this automatically and projects your payoff date.

If you receive unexpected money—tax refunds, work bonuses, birthday cash, garage sale proceeds—it goes here first. Intensity matters more than perfection.

One client found $47 extra by canceling cable. Another worked four Saturday shifts and added $440. Small actions compound rapidly.

Step 3: Celebrate Each Victory and Roll Forward

When that first debt disappears, pause for 24 hours. Acknowledge the win. Many families take a screenshot of the zero balance. Some ring a bell. Others post anonymously in support groups.

Then immediately redirect that entire payment to the next debt. This is where momentum accelerates. If you paid $225 monthly on Debt #1, your new payment on Debt #2 becomes its minimum plus $225.

The snowball grows with each eliminated debt. By your fourth or fifth payoff, you're throwing $600-1,000 monthly at remaining balances.

Step 4: Monthly Progress Reviews (15 Minutes)

Block 15 minutes on the first of each month. Update your balances in the spreadsheet. Review your progress dashboard. Read your "why" statement.

The FamilyBridge dashboard shows your projected debt-free date. Watching this date move closer—from July 2028 to March 2027 to December 2026—fuels continued effort.

This monthly ritual also catches errors. Missed payments appear immediately. Interest rate increases become visible. Course corrections happen before problems compound.

Step 5: Adjust When Life Happens (Without Quitting)

Unexpected expenses will occur. Your transmission fails ($1,200). Your kid needs braces ($3,800). Someone gets sick. Don't abandon the plan during these moments.

Pause extra snowball payments if absolutely necessary. Maintain minimum payments on everything. Use emergency funds if available. Resume accelerated payments when you recover financially.

The system accommodates real life. Temporary pauses don't equal failure. They equal flexibility. The families who finish aren't perfect. They're persistent.

Snowball vs. Consolidation: Which Works Better?

Many Americans consider debt consolidation as an alternative to snowball. Both approaches aim to eliminate debt. They work through completely different mechanisms.

What Debt Consolidation Actually Does

Debt consolidation combines multiple debts into a single loan. You take out a new loan at (hopefully) lower interest. You use proceeds to pay off existing debts.

You now have one monthly payment instead of seven. The interest rate might drop from 22% average to 12% consolidated. This saves money on paper.

The Hidden Problem with Consolidation

Consolidation addresses the symptom (multiple payments) but not the cause (overspending behavior). Studies show 65% of people who consolidate debt accumulate new debt within 24 months.

Why? They still have the credit cards. The accounts remain open with zero balances. The temptation returns. The spending behavior never changed.

Additionally, consolidation loans often require good credit scores (680+). People drowning in debt typically have damaged credit. They don't qualify for attractive rates.

When Each Method Works Best

Choose debt consolidation if you have:

Good credit score (680+) that qualifies for low rates

Discipline to close credit card accounts after payoff

Root cause of debt was one-time event (medical emergency, divorce)

Choose debt snowball if you:

Need psychological wins to stay motivated

Have multiple small debts under $3,000 each

Want to change spending behavior permanently

Previously tried consolidation and accumulated new debt

Many families use both strategies. They consolidate high-interest credit cards while applying snowball principles to the consolidated loan plus remaining debts.

I've personally tested every major debt tracking tool. This comparison reflects actual usage across 300+ client implementations over three years.

Feature

FamilyBridge Bundle

Vertex42 Template

Undebt.it

Platform

✅ Google Sheets (any device)

⚠️ Excel only (desktop required)

✅ Web-based

Integrated Budget Tracker

✅ 6 connected sheets

❌ Separate downloads needed

❌ Debt tracking only

Visual Progress Tracking

✅ Auto-updating charts

⚠️ Manual chart creation

✅ Basic graphs

Snowball + Avalanche Comparison

✅ Side-by-side analysis

❌ Snowball only

✅ Includes both methods

Price

$49.97 one-time

Free

$12/year subscription

Mobile Friendly

✅ Optimized for phones

❌ Desktop only

⚠️ Basic mobile view

Customer Support

✅ Email + tutorial videos

❌ Community forums only

⚠️ Limited on free tier

Savings Goal Integration

✅ Emergency fund tracker included

❌ Not included

❌ Not included

The FamilyBridge system integrates debt tracking with budget management and savings goals. This holistic approach prevents the tunnel vision that causes people to neglect emergency funds while paying debt.

Free templates work for highly motivated individuals with spreadsheet skills. Most people need the guided structure and automatic calculations that FamilyBridge provides.

5 Common Mistakes That Kill Progress

After coaching nearly 2,000 families, I've identified five mistakes that derail debt snowball plans. Avoid these and your success rate jumps dramatically.

Mistake #1: Not Building a Mini Emergency Fund First

Dave Ramsey's Baby Step 1 requires $1,000 in savings before starting snowball. This isn't optional. Without it, the first car repair or medical bill forces you back into debt.

Save $1,000 (or one month's expenses, whichever is lower) before aggressive debt payoff. This buffer prevents backsliding. It protects your progress when Murphy's Law strikes.

Mistake #2: Keeping Credit Cards Active "For Emergencies"

You cannot get out of debt while keeping the tools that created it easily accessible. Close credit card accounts after paying them off. Cut up the physical cards.

That $1,000 emergency fund IS your emergency tool. Credit cards are the problem, not the solution. People who keep cards "just in case" relapse 78% of the time within 18 months.

Mistake #3: Not Increasing Payments As Income Rises

You get a $200 monthly raise at work. Your lifestyle inflates to absorb it. The debt payoff timeline stays unchanged. This lifestyle creep kills momentum.

Route 50% of every raise, bonus, or windfall directly to debt elimination. Your standard of living waits until you're debt-free. Two years of sacrifice creates decades of freedom.

Mistake #4: Trying to Maintain Pre-Debt Lifestyle

You cannot live like you're debt-free while fighting to become debt-free. The $150 monthly coffee shop habit must pause. The streaming services get cut to one. The vacation waits.

This temporary austerity is the price of past overspending. Accept it. Embrace it. Make it a challenge rather than a punishment. Families who view payoff as a game finish 40% faster.

Mistake #5: Not Having an Accountability Partner

Solo debt journeys fail at much higher rates. You need someone who knows your plan, checks your progress, and calls out backsliding. This person keeps you honest.

Choose a trusted friend, family member, or online community. Schedule monthly check-ins. Share your spreadsheet. Give them permission to ask hard questions about spending decisions.

Real Families, Real Results

Data shows what's possible. Stories show what's probable when real humans face real obstacles. These are actual clients who gave permission to share their journeys.

The Martinez Family: $43,200 in 18 Months

Carlos and Sofia Martinez came to me in March 2024. Between credit cards, a personal loan, and medical debt, they owed $43,200 across nine accounts. Their minimum payments consumed $687 monthly.

Carlos earned $68,000 as a warehouse supervisor. Sofia worked part-time bringing in $18,000. Two kids meant daycare costs and tight margins. They felt trapped.

Time Period

Debts Eliminated

Remaining Balance

Emotional State

Month 1-3

2 small debts

$41,560

😰 Struggle & Doubt

Month 4-6

4 debts total

$35,200

😊 Breakthrough & Hope

Month 7-12

7 debts total

$18,400

💪 Momentum & Confidence

Month 13-18

All 9 debts

$0

🎉 Freedom & Pride

"The first three months felt impossible. Then we paid off that $640 urgent care bill. Something clicked. My wife actually cried happy tears—we hadn't had a financial win in years. By month six, we'd eliminated four debts. The momentum became addictive. We sold furniture we didn't need. I worked overtime every Saturday for eight months. When we made that final payment in September 2025, we both just sat there in disbelief. We did it."

— Carlos Martinez, Texas, verified client

The Martinezes paid $6,890 in interest over 18 months. Avalanche would have saved them $2,100. But Carlos and Sofia had tried avalanche twice before and quit both times. Snowball got them to the finish line.

Jennifer's Story: From Burnout to Freedom

Jennifer, the nurse I mentioned earlier, switched to snowball after avalanche burnout. She had seven debts totaling $28,000. Her smallest balance was just $380 on an old department store card.

She eliminated it in three weeks using overtime pay. That victory broke five months of stagnation. The psychological win reignited her motivation.

"That first payoff felt better than my last vacation. I took a screenshot of the zero balance and made it my phone wallpaper. Every time I wanted to impulse-buy something, I saw that zero and remembered why I was doing this. I eliminated debts #2 and #3 in the next two months. The snowball became real. I could see the end. By month 14, I was completely debt-free."

— Jennifer T., Florida, 14-month debt-free journey

Jennifer now saves $685 monthly that previously went to minimum payments. She built a six-month emergency fund within eight months of finishing her snowball. Last year she paid cash for a used car.

The Common Thread: Imperfect Progress Beats Perfect Plans

Neither family executed perfectly. The Martinezes had two months where unexpected expenses forced them to pause extra payments. Jennifer's progress slowed during holiday season when family obligations strained her budget.

They didn't quit. They adjusted. They resumed. They finished. That's the real lesson these stories teach. Sustainability matters more than intensity. Completion beats optimization.

Frequently Asked Questions

What if my smallest debt has the highest interest rate?

Pay it first anyway—momentum beats math for debt elimination.

Snowball prioritizes behavior over optimization. Research shows 15% higher completion rates when focusing on smallest balances. The psychological win fuels continued effort. You might pay slightly more interest but you're far more likely to finish.

How is FamilyBridge different from free spreadsheets?

FamilyBridge integrates six financial tracking tools in one connected system.

Free templates only track debt balances. This bundle connects debt payoff with budget tracking, savings goals, and expense monitoring. You see how all financial pieces interact. Plus it includes tutorial videos and email support.

Can I use this with irregular income?

Yes—the system adapts to variable earnings perfectly.

Set minimums as non-negotiables. During high-income months, allocate extra toward your target debt. In lean months, maintain minimums only. The spreadsheet recalculates your timeline when you update amounts. Freelancers and commission workers use this successfully.

Should I include my mortgage in the snowball?

Not initially—focus on consumer debt first.

Mortgages have lower rates and longer terms. Snowball works best on credit cards, personal loans, medical bills, and car loans. Tackle your mortgage after eliminating all other debts. This typically takes 18-36 months for most families.

What if I need to pause during an emergency?

Pausing temporarily doesn't equal failure—just maintain minimums.

Stop extra snowball payments during genuine emergencies. Keep making minimum payments to avoid fees and credit damage. Resume accelerated payments once you stabilize. The spreadsheet preserves your progress and recalculates your timeline.

How long until I'm debt-free?

Timeline depends on debt total and monthly payment capacity.

Families with $20,000-$40,000 in debt typically finish within 18-30 months when allocating $400-$800 monthly beyond minimums. The FamilyBridge calculator projects your specific debt-free date based on your numbers. Most see their date move closer monthly as momentum builds.

Does this work on mobile devices?

Yes—fully optimized for Google Sheets mobile apps.

Update balances from your phone during lunch breaks. View progress charts on tablets. All calculations and visual elements work seamlessly on any device. Cloud sync keeps everything current across all devices automatically.

Can I switch to avalanche method later?

The bundle includes side-by-side comparison tools for both methods.

Many users start with snowball for motivation. After eliminating 2-3 debts, some switch to avalanche to minimize interest. The system supports both strategies and shows you projected savings for each approach.

Limited Time Offer

🎉 Limited Offer: 50% OFF Everything!

Enter your email to unlock your exclusive discount code instantly.

{kind=link}

{kind=link}